It is inevitable that reorganisation of ownership structure will make business sense at some point in a business’ lifecycle as a result of evolving plans, tax law changes, lifetime events etc. What that ‘reorganisation’ looks like will take different forms for different purposes. It may be required at one, or even multiple, junctures along the way.

In our latest blog, we explore three of the more common ‘regular’ revisions of structure, namely:

- Incorporations (and dis-incorporations)

- Holding company insertions (and divisionalisations)

- Demergers and partitions

Incorporation

(and dis-incorporation)

After a significant and consistent trend, over the last 20 years or more, in favour of using the limited company ownership structure as the preferred vehicle for doing business, the incidence of incorporations is arguably not as significant as it was previously. However, incorporation remains an important option for owners operating as sole traders or partnerships and continues to offer businesses (in particular, those early in their lifecycles) the first key revision of status.

Transition from unincorporated business to a limited company, in its various forms, can present the owner(s) with considerable commercial, legal and taxation benefits. These are outlined in our blog The Tax Merits of the Limited Company (5 November 2019) and do not need to be repeated here.

Dis-incorporation is also a positive option for some limited companies in specific circumstances. We do not take it for granted that the limited company is right for all, at all times.

Holding company insertion

(and divisionalisations)

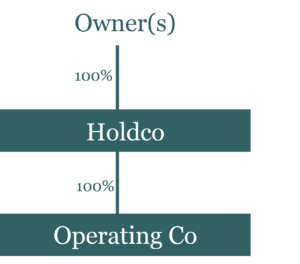

While many privately-owned businesses are conducted through a singleton operating company, it is increasingly common for owners to opt for a holding company (“Holdco”) structure as depicted below, and to have that holding company inserted as part of a tax-free reorganisation.

With a “Holdco” structure like this we can move principal assets (cash, property, IP) up to the holding company and away from the commercial risks faced by the operating company. We can do this at zero taxation cost.

Along the way, it is commonly the case that we might establish significant share capital in Holdco, helping to convey the substance of the group to the outside world and also providing a convenient facility for potential future share exits (for one or more shareholders) by rights of “share capital reduction”, which can be both flexible and stamp duty efficient.

Owners should further note that this structure opens up greater flexibility for a future sale of the business.

A buyer might buy the whole group (i.e. the shares in Holdco) for a one-tier taxed disposal of the business – or, owners might sell the operating company out of Holdco for a tax-free sale at that point (thanks to what is known as the “substantial shareholding exemption”). This can be powerful where the plan is to retain value in a corporate entity for ongoing investment, for paying down debt, for new ventures, for passing down to family, etc.

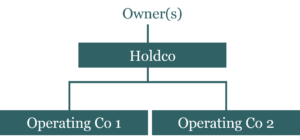

Expanding on the “Holdco” structure, it is sometimes appropriate to establish the new holding company and to create a structure with “sister” operating companies, as depicted here:

In addition to the features referred to above, this revision of structure facilitates the “separation” of different activities within a tax-advantaged group. That separation provides:

- protection

- ease of incentivisation (of key personnel)

- management

This structure also lines up the possible sale of one or other, out of Holdco, tax-free (as noted above).

For those operating separate operating companies outside a “group” structure like this, the various group reliefs achievable for taxation are foregone, of course.

Demerger and partition

From time to time a company or existing group needs to undergo some form of “demerger” of its activities, into two or more pieces. While a lot of the same objectives as those illustrated above are served by demerger, splitting a business structure into two or more pieces often derives from the need to “partition” the activities/assets between different parties.

Partition might be desirable for a host of reasons including, by way of examples only:

- Separate focus on different activity

- Dispute between owners

- Carve-up between family members needing independent control

- Legal requirements, e.g. to avoid conflicts

Demergers (including partitions) can be achieved by a range of methods from which the most appropriate needs to be selected for the specific circumstances of the business in question.

These methods include:

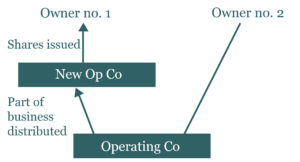

(i) The “statutory” demerger

Specific conditions need to be met to allow for a statutory (or “direct”) demerger like this, one which allows part of a business to be distributed free of tax to a new entity to be carried on, typically, by one or other of the owners of the existing operating company.

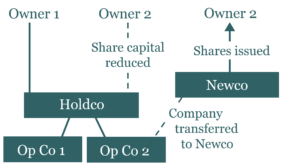

(ii) Indirect demergers

Splitting up existing companies or groups on an “indirect” basis typically involves a number of steps in part of a process designed to fall inside the reorganisation/reconstruction rules within the tax code. Reduction of share capital or a liquidation of a temporary Holdco are common methods of achieving the desired demerger/partition on a tax-free basis.

How can we help?

Structure, and the revision of structure, is important throughout the life of business. Getting structure right serves commercial, legal, financial and domestic objectives. As a result, it is very important to keep on the agenda throughout the life cycle and to seriously consider revising when the circumstances dictate.

Reorganisation of business ownership structure is part of Harold Sharp’s specialist advisory services. If you would like to discuss whether it might be appropriate for you and your business, please email tax@haroldsharp.co.uk or telephone 0161 905 1616.